2017 Year-End Forecasts

Wells Fargo Investment Institute has revised its guidance, expecting increased economic growth and inflation.

2.3%

U.S. Gross Domestic Product (GDP) growth

2.4%

U.S. inflation (CPI)

2,230–2,330

S&P 500 Index

1.25–1.50%

Federal Funds Rate

Source: Wells Fargo Investment Institute, May 31, 2017. Subject to change.

Investment and Insurance Products: NOT FDIC InsuredNO Bank GuaranteeMAY Lose Value

Increased Opportunities Ahead

Paul Christopher, Head Global Market Strategist for Wells Fargo Investment Institute, discusses what may be ahead in equities, fixed income, and other asset classes.

Key Highlights

In the first half of 2017, slow but steady global economic growth sparked significant gains across many asset classes, and investors anticipated new U.S. policies would drive further economic growth. But recurring political and economic shifts, such as those related to European populism and China’s economic reform challenges, continue to be a concern for financial markets.

Click on any of the links below to go to that section of the report for more information.

-

A First-Half Recap: Optimism, Then Uncertainty

There have been three distinct phases of the market so far in 2017.

-

Economic & Investment Outlook

Our take on the current and projected trajectory of the economy and investment markets.

-

Recommendations for the Second Half of 2017

Market conditions help drive our strategic recommendations for your portfolio.

A First-Half Recap: Optimism, Then Uncertainty

During the first half of 2017, we’ve seen three distinct phases of market returns.

Economic & Investment Outlook

Forward Motion Appears Intact

U.S. economic growth and inflation began the year on a weak note, but strengthening data on orders for new production point to steady economic activity in the second half. Economic growth now has broadened to include Europe, Asia, and Latin America.

Positives:

- We expect further economic improvement in the Eurozone over the next 12 months, which could reinforce global confidence.

- A combination of steady economic growth and restrained inflation should allow central banks to focus on removing their extraordinary monetary stimulus.

- U.S. job gains should continue at a moderate pace.

- Household and business borrowing trends show none of the exuberance that typically takes place in advance of a recession (see chart).

Risks to Our Outlook:

- If the U.S. were to impose punitive tariffs on other countries, it could increase U.S. inflation and hurt companies with international supply chains.

- China could move too aggressively to consolidate its Industrials sector, precipitating a broader slowdown in global trade, commodity prices, and inflation.

- Nationalist policies, such as trade restrictions, could be negative for earnings and could sharply inflate prices and borrowing costs.

Consumer Debt and Mortgage Payments Have Declined From Recent Highs

Low interest rates have helped reduce consumer debt and household mortgage payments, supporting household cash flow.

Drag handles at top to zoom in on a specific time period.

Sources: Bloomberg, the Federal Reserve, and Wells Fargo Investment Institute

The data show estimated minimum consumer debt payments and minimum mortgage principal and interest payments as a percent of disposable income. Disposable income is after-tax income, calculated by the U.S. Bureau of Economic Analysis. Dates: March 31, 1980, through December 31, 2016.

Continued U.S. Earnings Growth, Stretched Valuations

We expect stronger revenue and earnings growth for S&P 500 Index companies. A healthy consumer should continue to support growth in a variety of cyclical sectors, while expansion in developed international economies should benefit large multinational companies.

Positives:

- Increased capital spending as the domestic and international economies expand simultaneously should drive later-cycle U.S. earnings for the Industrials sector.

- The Financials sector should benefit from a combination of modestly higher spreads, continuing lending growth, and potential regulatory revisions.

- Lower valuations and some signs of economic stabilization helped international markets.

- Stability and incremental economic growth in emerging markets sparked outperformance in the first half of the year (see chart).

Risks to Our Outlook:

- At current valuations, volatility is likely to rise as the Fed slowly raises rates.

- The U.K.’s exit from the European Union could prove an unexpectedly large headwind to growth.

- China’s growth could slow if Beijing resumes a determined approach to implementing reforms.

A Strong Start for International Equities

Developed and emerging equity markets outperformed the main U.S. indicies in the first few months of 2017.

Click or tap on an item in the legend to toggle the line on or off. Drag handles at top to zoom in on a specific time period.

Chart represents index level in 2017; values are indexed to zero at year-end 2016.

Sources: Thomson Reuters Baseline, Wells Fargo Investment Institute. Dates: December 30, 2016, through April 20, 2017. An index is unmanaged and not available for direct investment. Past performance is no guarantee of future results.

Stay Focused Amid Change

In the first half of 2017, the Fed raised expectations for the number of interest-rate hikes in 2017 and began discussing the possibility of balance sheet reductions. Bond prices reacted as investors added or reduced risk based on sentiment and economic developments.

Positives:

- Our 10-year Treasury yield target range is 2.25% to 2.75%, an increase of 0.25%. Our 30-year Treasury target yield range is 3.0% to 3.5%, also increased by 0.25%.

- Slightly higher Treasury yields and three rate hikes this year are unlikely to create lasting bond market disruptions.

- We favor moving up in credit quality, as high-yield spreads over U.S. Treasuries are unusually tight (see chart).

Risks to Our Outlook:

- After steepening in late 2016, the yield curve flattened over the first half of 2017. Additional curve flattening would be a risk to our fixed-income targets and to our call on continued economic growth.

- The number of potential changes in Fed leadership could create uncertainty, which is rarely good for the bond market.

- A stronger U.S. dollar and higher global rates are significant headwinds to international developed fixed-income markets.

Narrower Yield Differential Between High Yield and Treasury Securities Brings Risk

The yield differential (or spread) between bonds in the Bloomberg Barclays U.S. Corporate High Yield Bond Index and comparable Treasuries was below the long-term average for the yield spread.

Drag handles at top to zoom in on a specific time period.

Sources: Bloomberg and Wells Fargo Investment Institute

Dates: August 15, 2005, through April 17, 2017. One basis point is equal to one-hundredth of one percent, or 0.01 percent. One percent equals 100 basis points. Chart measures values from beginning and middle of each month. Past performance is no guarantee of future results.

Commodities Should Trade Within Defined Ranges

Commodities remain stuck in a bear-market super-cycle. During the first half of 2017, real assets generally performed as expected — commodities underperformed, Master Limited Partnerships (MLPs) performed like the market, and Real Estate Investment Trusts (REITs) outperformed.

Positives:

- Agriculture offers the best long-term potential of the various commodity sectors.

- REIT fundamentals remain relatively sound, and we expect them to stay that way for a few more years. REIT valuations look attractive compared with most other yield-based investments. We prefer U.S. REITs to global REITs.

Risks to Our Outlook:

- Oil and gold both remain swamped in excess supply, limiting their price.

- If interest rates quickly move higher, REITs could suffer.

- The upside on MLPs is likely to be capped, which could add volatility.

A Look at Past Commodity Super-Cycles

Bear-market super-cycles tend to be longer-lived than bull-market super-cycles. History suggests we have some years left in this current bear super-cycle.

Drag handles at top to zoom in on a specific time period.

Shading indicates commodity bear markets.

Sources: Bloomberg and Wells Fargo Investment Institute. Monthly data: January 1860 through March 2017.

Dates selected show available data on commodity bear markets since 1860. Commodity Composite Index measures a basket of commodity prices as well as inflation. It blends the historical commodity index from George F. Warren and Frank A. Pearson; the U.S Bureau of Labor Statistics (BLS) Producer Price Index for Commodities (PPI–Commodities); the National Bureau of Economic Research (NBER) Index of Spot Market Prices of 22 Commodities; and the Reuters Continuous Commodity Index. Past performance is no guarantee of future results.

A Better Day for Active Management

For alternative investments, the postcrisis regime created challenges for active management. A decline in correlations among assets and a better opportunity to generate excess returns from long and short positions is part of the new era for alternative investments, one that we anticipate will remain in place for the foreseeable future.

Positives:

- We have observed a broad-based improvement in hedge fund performance over the past 12 months.

- Deteriorating balance sheets within the high-yield debt market may create opportunities for Long/Short Credit and, eventually, Distressed Credit strategies.

- Tactical strategies like Relative Value and Equity Hedge should benefit from higher equity and fixed-income volatility.

Risks to Our Outlook:

- A return to the postcrisis era, marked by quantitative easing and high correlations among asset classes, would cause a risk to our outlook.

- Deterioration in consumer credit or commercial real estate could affect Structured Credit or commercial mortgage-backed securities (CMBS).

Alternative investments, such as hedge funds and private capital funds, are not suitable for all investors. They are available only to persons who are “accredited investors” or “qualified purchasers” within the meaning of the U.S. securities laws.

Hedge Fund Returns Began Normalizing in 2016

We believe the increases in interest rates and inflation that began in 2016, coupled with less focus on U.S. monetary stimulus, resulted in stronger performance for hedge funds.

Drag handles at top to zoom in on a specific time period.

Sources: Bloomberg and Wells Fargo Investment Institute

Dates: January 1, 1990, through April 1, 2017. The HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to HFR Database. An index is unmanaged and not available for direct investment. Past performance is no guarantee of future results.

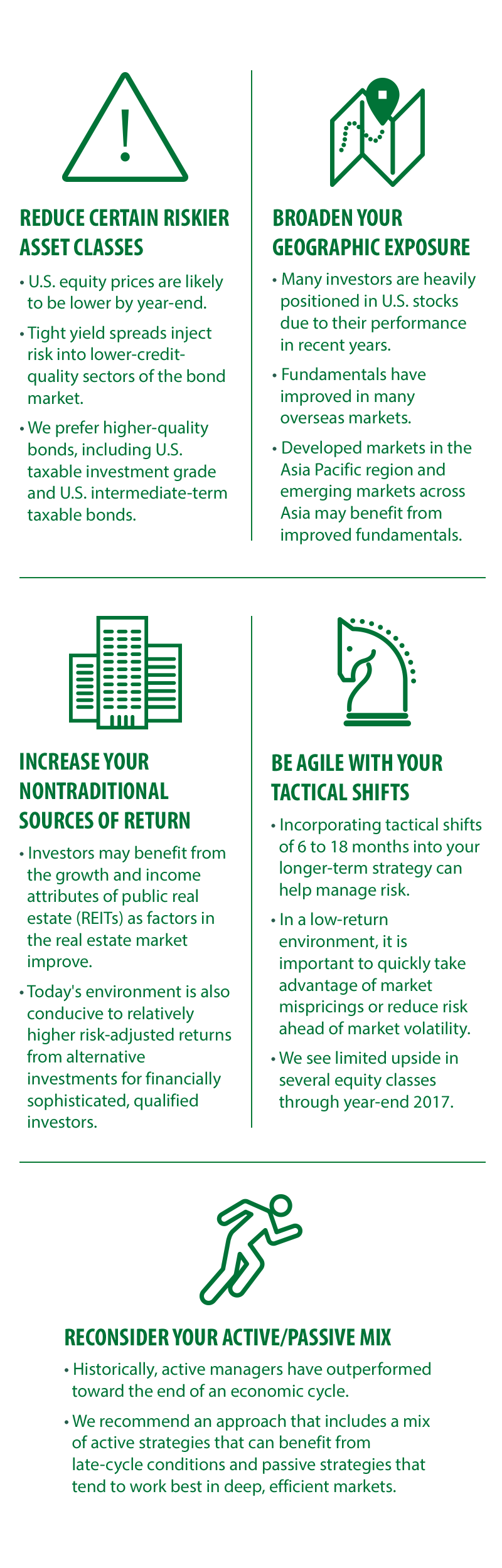

Top 5 Recommendations for the Second Half of 2017

We strongly believe that the foundational principles of investing, including diversification, globalization, and portfolio rebalancing, are vitally important in today’s markets. Here are the portfolio recommendations we think will be critical to investor success in the second half of the year.

Investment Expertise and Advice to Help Clients Succeed Financially

Wells Fargo Investment Institute is home to more than 100 investment professionals focused on investment strategy, asset allocation, portfolio management, manager reviews, and alternative investments. For additional information on Wells Fargo Investment Institute, visit our website.

Read the Full Report

Click or tap ‘View Report’ to get the full version of our 2017 Midyear Outlook.